Back

February 14, 2025

Real World Assets and their tokenization potential captured the attention of institutions and crypto enthusiasts alike, unifying them in the common pursuit of seamless transactions protected by code—and the ability to access any asset, however liquid or illiquid, however esoteric or luxurious, and however risk-free or risky, using tokens.

From tokenizing real estate to luxury cars, from treasury bills to money market funds, and from equities to household loans, several institutions and startups have enthusiastically embraced the tokenization narrative. Market reports have since emerged with wildly divergent estimates. An oft-cited projection from BCG envisions $16 trillion in tokenized assets by 2030, yet McKinsey’s forecast sits at around $2 trillion, while Standard Chartered and Finpulse anticipate a ~$30 trillion market by 2032.

TokenFi, on the other hand, tends to echo BCG’s numbers. Despite these ambitious forecasts, data from RWA.xyz indicates that the current tokenized asset market stands at a mere $17 billion (excluding stablecoins) or about $240 billion (including stablecoins). This suggests that to reach even the modest lower bound, the market would need to grow at a compound annual rate of roughly 42% over the next six years—with the higher forecasts requiring unsustainable year-on-year growth of ~123%. In short, the “golden goose” that both traditional institutions and crypto-hodlers expected has yet to hatch its full potential.

The following sections delve into why this is so—and what hurdles remain.

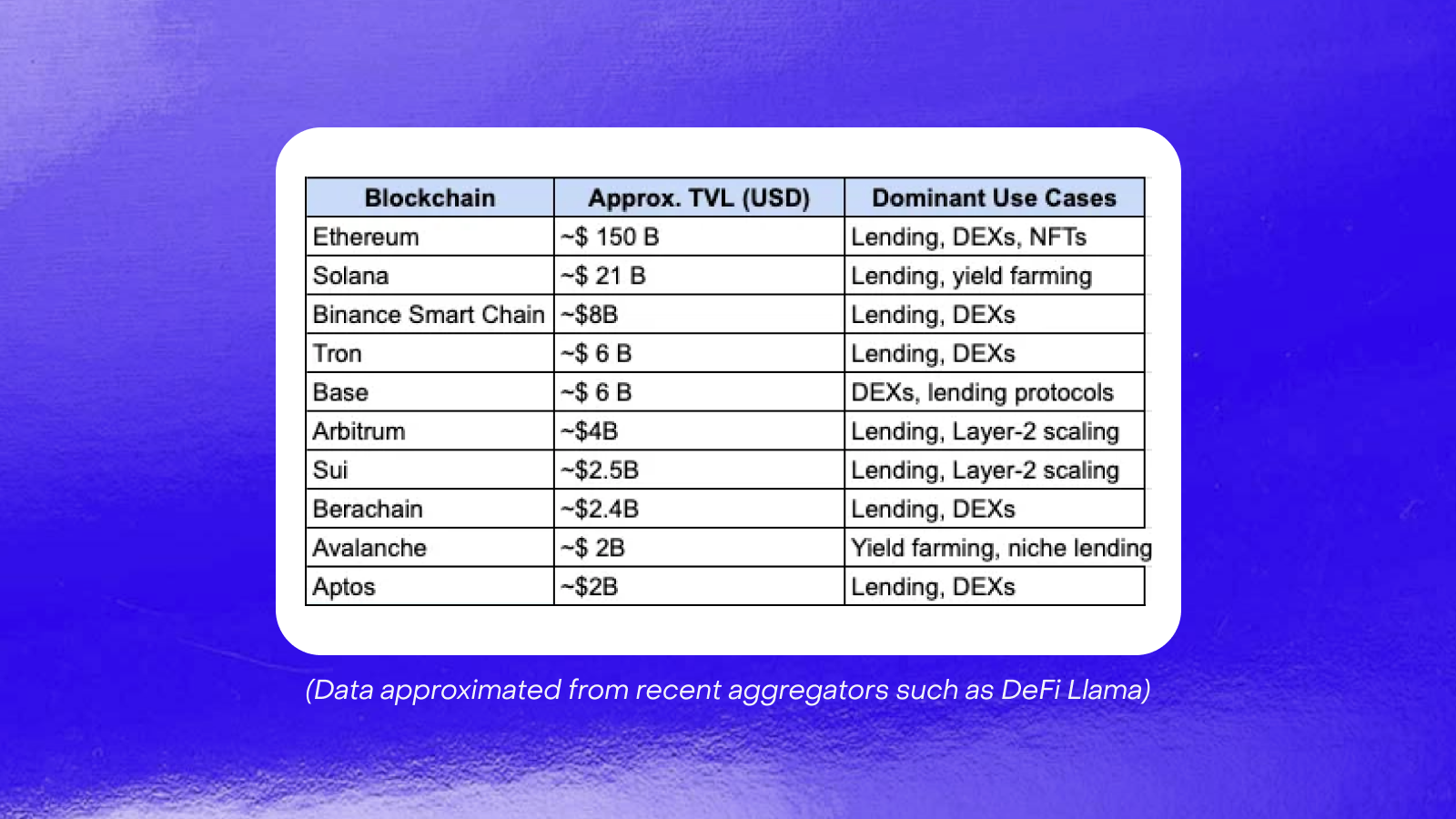

While the decentralized finance (DeFi) ecosystem currently commands a total value locked (TVL) of roughly $100 billion, this figure belies the extreme fragmentation and concentrated use cases across blockchains. The DeFi landscape is defined by a few dominant chains that cater to lending, decentralized exchanges (DEXs), and yield farming. Consider the approximate breakdown below:

On the yield front, DeFi platforms offer a dazzling array of opportunities—from staking rewards and using staked assets as collateral to taking loans for leveraged trading. For example, Aave’s market data (viewable at Aave Markets) highlights yield ranges that often exceed what traditional tokenized asset offerings can promise. In contrast, tokenized asset platforms like BUIDL typically offer yields in the 4% range. The allure of higher returns in DeFi is tempered by increased risk and fragmentation of liquidity, meaning that even with impressive yield numbers, the underlying pie is too small and scattered among numerous protocols.

This fragmentation not only dilutes liquidity but also concentrates risk in silos—limiting scale, interoperability, and ultimately, mainstream adoption.

Tokenization theoretically enables anyone, anywhere, to own a fraction of a real-world asset. However, the legal transformation of a token into recognized ownership of the underlying asset remains a complex challenge. In many jurisdictions, the rights conferred by a digital token do not automatically translate into legal rights over physical assets.

Consider an asset located in an emerging market such as Vietnam or India. Instead of granting direct legal title via a token, many projects route the asset into a Special Purpose Vehicle (SPV) domiciled in a jurisdiction with clearer tokenization frameworks—such as Singapore. In this structure, the token represents an indirect claim on the asset through the SPV’s share register. While this workaround addresses some regulatory concerns, it also creates a layered, and at times opaque, chain of legal rights. Should the underlying asset default or require recovery, the complexity of cross-jurisdictional enforcement becomes a significant roadblock.

Thus, while tokenization is universal in theory, legal recognition remains fragmented by national and regional laws—a point of skepticism for both institutional investors and crypto enthusiasts.

Success in the tokenized asset space depends not solely on technology but on the broader ability to originate, distribute, and lend against these assets.

Effective origination requires jurisdictional approval and a strong relationship with local authorities. For example, the tokenization of house ownership—as attempted by players like Figure Markets—demands not only technical innovation but also alignment with local property laws and regulatory frameworks. Figure Markets, for instance, has introduced DART (Digital Assets Registration Technologies), which competes with MERS, a technology owned by ICE, which also owns NYSE. Without these “jurisdictional blessings,” even the most elegant blockchain solution can flounder.

The current DeFi infrastructure, with its $100 billion TVL, is too fragmented to serve as the sole channel for distributing tokenized assets. Instead, distribution for any given asset will continue to rely on traditional mechanisms: personal relationships, face-to-face sales, boardroom negotiations, and exclusive dinners. Here, tokenization is merely an incidental benefit—a cost-reduction tool aimed at streamlining middle and back office functions. The true challenge is to integrate these conventional channels with on-chain efficiency, a task that remains largely unsolved.

Lending against tokenized assets also faces hurdles. The collateral quality, valuation uncertainties, and legal ambiguities mean that financial institutions remain wary of fully embracing tokenized loans. The capacity to originate and distribute assets, coupled with a robust lending framework, will likely determine which players ultimately succeed in this nascent market.

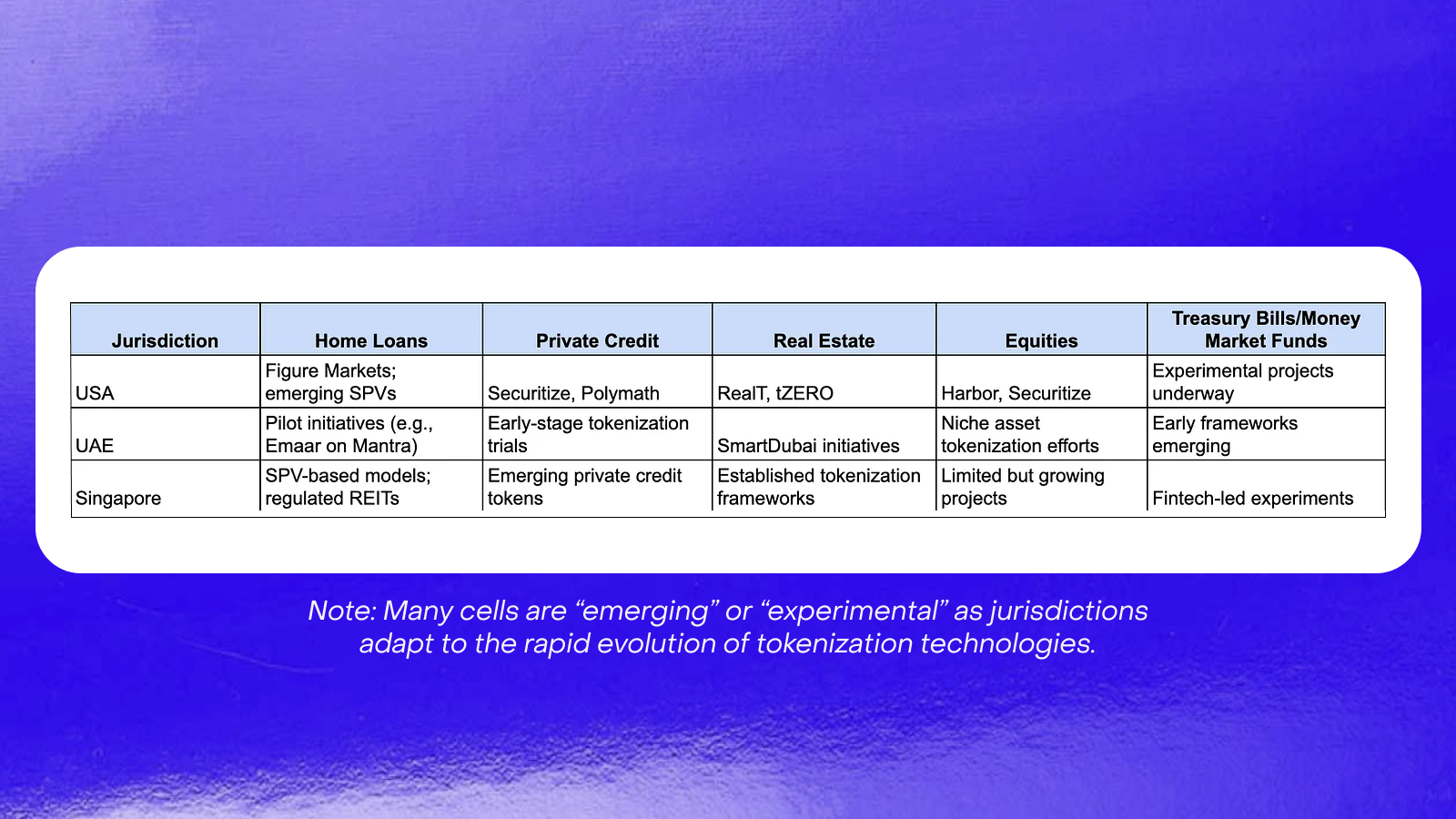

A glance at the current landscape reveals a patchwork of initiatives, each tailored to specific asset classes and regulatory environments. The following table provides an illustrative (if not exhaustive) asset–jurisdiction matrix:

This matrix underscores the reality that while tokenization technology may be universal, success hinges on localized solutions tailored to each jurisdiction’s legal, cultural, and economic environment.

Underwriting in blockchain ecosystems tends to rely on consensus mechanisms—a feature that works well for public assets but falters when applied to real-world assets. Protocols such as Centrifuge, Compound, and Maple Finance have experimented with decentralized underwriting, using risk capital to back loans against tokenized assets. However, the data flow from off-chain sources to on-chain protocols remains problematic, particularly for illiquid or complex assets like real estate.

Reliable underwriting demands robust oracles and a “single source of truth” data layer that accurately captures the current state and valuation of underlying assets. Without this, the value mapping of tokenized assets remains imprecise—a critical shortfall in an industry that prizes transparency and reliability.

Envision a future where the technology and legal frameworks coalesce to create a seamless ecosystem for tokenized real-world assets:

Despite the hype and the transformative promise of tokenizing real-world assets, the current market remains a crowded and fragmented space. The twin challenges of scaling DeFi TVL and bridging the legal gap in asset ownership mean that consolidation is inevitable. In time, winners will emerge—players who can seamlessly originate, distribute, and lend against tokenized assets across every jurisdiction. Until then, the road ahead, though promising, is paved with significant challenges that demand both technological innovation and regulatory finesse.