Back

February 3, 2025

The last couple of years have been transcendental in their ability to enable traditional finance acceptance of crypto as both an asset class, with a reinforcement of its fundamentals.

Among several other developments, the key political tailwinds that shaped the space over the last few months include:

While all of these are non-statistical pieces of news information, the overall narrative is one of increasing crypto regulatory acceptance across the US, and the legitimization of the asset class, with the president himself quashing the ‘commodity vs security’ debate by launching $TRUMP, which is positioned as a highly speculative security (aka, a means to raise money that Trump and Co. benefit the most from).

The above background strengthens a narrative that has been dominant for 5+ years now — the arrival of Wall Street on crypto. While the watershed moment for this occurred over a year ago with the BTC ETF being approved (with BTC being treated as a commodity and not a security). The ETF offerings have scaled vastly, with the market cap reaching $ 125 B across ETFs.

The fees from just the ETF offerings across all the ETFs currently presents represents about $ 550 Mn. These have also rapidly and vastly outpaced the long-standing ETF offerings of several firms. (For instance, iShares and Vanguard’s S&P 500 ETFs have an AUM of ~$ 500 Mn - $ 600 Mn in comparison)

Due to erstwhile rigid regulatory stances, and the SEC’s mandate to treat digital assets as liabilities on the balance sheet, the market participation of traditional finance in the space has been limited primarily to leveraging cryptocurrencies as a trading instrument, and a potential yield-bearing instrument (in the case of Ethereum).

However, the changing world order in the space expands the roles and games that Wall Street and the banks could play in the ecosystem.

The crypto ecosystem emerged with a strong ethos of “trustlessness,” largely due to the volatility of early market participants and the desire to bypass traditional intermediaries. In reality, however, trust in established financial institutions remains central to global finance. We see this in the rise of Bitcoin ETFs — offered and custodied by familiar banks, accessible via standard brokerage accounts — and in new regulations requiring a clear separation of custodial services from exchange operations.

While the debate rages on about institutional custody being against the spirit of the crypto ecosystem (read more about it here), the fact remains that self custody is cumbersome and inconvenient, with a point of failure that is reliant on the user’s own ability to secure a set of random words. In a world where most people rely on password managers and familiar banking interfaces, delegating crypto custody to a recognized financial institution feels both practical and familiar. Early movers such as LBBW have already partnered with crypto-asset custodians such as Bitpanda to offer custodian services to their clients (source). Conversations with leading MPC scientists and wallet infrastructure providers also indicate several potential bank contracts in the space.

Why banks? They already safeguard your salary and other assets. Handing them your Bitcoin, Ethereum, or stablecoins can seem like a logical extension — especially if the institution is perceived as “too big to fail.”

That said, digital assets can be more complicated than fiat. Traditional banks often can’t lend volatile assets as effectively as cash, so custody fees may replace the interest you’d normally earn. Fiat-backed stablecoins, however, present a different dynamic. Their relative price stability could allow banks to generate yield, much like short-term money market funds or deposit-based lending.

Looking ahead, as the market deepens and blue-chip crypto assets become less volatile, banks may develop lending products, derivatives (akin to CDOs), and other yield-generating mechanisms on top of these tokens. Yet we’ll likely see restrictive loan-to-value ratios, higher collateral requirements, and robust regulatory frameworks around credit counterparty risks.

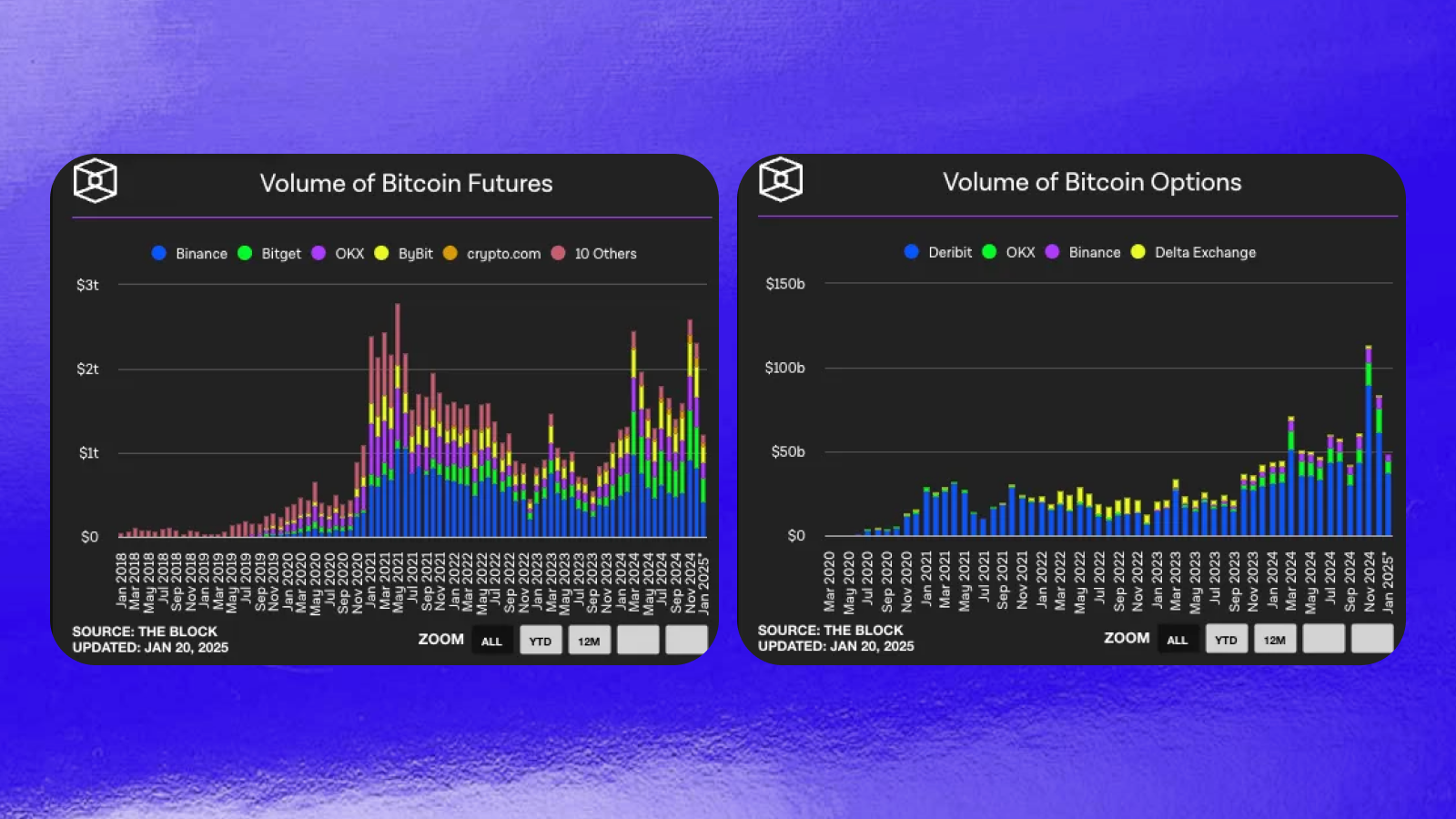

In the absence of existing traditional finance infrastructure such as market makers and clearing houses, early crypto adopters came up with an innovation called perpetuals to attain leverage on spot crypto assets. The volume for perpetuals has long overtaken the volume for spot crypto buying, reaching $ 2 Trillion for only Bitcoin as early as January 2021. Perpetuals are futures that leverage a funding rate mechanism to tie the future price to the spot price at fixed time intervals (longs pay shorts every 4-6 hours if the future price is higher than the spot price and vice versa).

Given the lack of market depth, options, however, have not seen large volumes in crypto so far. For instance, as evidenced below, when BTC futures volume was $ 2.7 trillion in May 2021, the corresponding options volume was a measly $ 21 Bn, accounting for <1% of the perps market. In contrast, the volumes of BTC options in December 2024 were $ 84 Bn vs a perpetuals volume of $ 2.3 Trillion.

Options have steadily grown from <1% of the BTC perp market (which remains the largest by volume in terms of the three instruments) to about 5% of the perps market. The argument, here, however, is that options volume is an indication of instiutional dominance in the space, and the increase of options volume signifies larger institutional entries into the space.

While plain vanilla options are interesting, additional instruments are likely to dominate future trades including funding rate swaps (to leverage the arbitrage in perpetual funding rates across different venues), and paves the way for the large scale adoption of other derivatives. These include credit default swaps built on collateralized assets, baskets of instruments, and complex structured products.

The lack of a standardized structure and large institutions to back markets as we know them resulted in several innovations in crypto ecosystems. These include automated market makers (which use hyperbolic curves to price assets in the absence of market makers in any market), and markets that operate 24x7, and report transactions on an immutable ledger, which makes transactions both final as well as transparent.

Traditional finance was built incrementally, with institutions building on top of institutions, with each institution being formed as a holder of “trust”. For instance, clearing houses are trusted organizations that allow large institutions to solve for counterparty risk in the case of leveraged trades. Crypto came up with mechanisms such as autoliquidations, and the smart contractization of liquidations to combat default and counterparty risks. This is primarily because the two stacks, traditional finance, and web3 are assumed to be built with the opposite assumptions of trust. Web3 strives to create trustless ecosystems, where traditional finance has always relied on trusted institutions.

That said, traditional finance has its fair share of illiquid high-ticket instruments that need liquid markets and efficient price discovery mechanisms. Automated market makers and smart-contract-based clearing houses could make escrow, price discovery, and the trading of illiquid assets that much easier.

Further, in a world where data collection is frowned upon, and companies pay large prices for spying on users, zero knowledge ways of sharing user information, and allowing them to be paid for being information sources does provide possibilities of a weirdly dystopian but fair world. There are several zk-identity solutions that have popped up over the last few years, with several governments now piloting blockchain based solutions to create Digital Identities, and to facilitate information sharing

The arrival of traditional finance also meant that traditional finance did what it would do to a new liquidity source —distribute the various existing instruments that they already have.

The arrival of several tokenized money market funds (read https://rwa.xyz for a more detailed breakdown) has implied that on-chain users have access to ownership in money market funds beyond borders. Countries have begun by tokenizing sovereign debt, with US T bills being followed by the sovereign debt of other countries such as Mexico and Euro bonds.

Other real-life instruments such as private credit have also made their way on-chain through various protocols such as Goldfinch, Maple, and Centrifuge among others.

However, the tokenization of real world assets is plagued by one overarching problem - making sure that the value on-chain constantly reflects the value in real life.

While this seems to be trivial for equities and other money market funds, traditionally illiquid instruments such as Real Estate and Private Credit need additional intermediaries and underwriters to make sure that the on-chain value reflects the best estimate of the off-chain value.

The critical gap that needs to be filled for mass adoption is the legal equivalence of tokens to ownership registers such as share registers. While certain jurisdictions already allow the tokenization of share registers such as Singapore’s MAS, equating the ownership of tokens to the ownership of the asset remains a cumbersome process.

Evolving regulation is likely to tackle this, while products with access to multiple jurisdictions, or a future agglomerator of various instruments across jurisdictions could smoothen the user experience further. Venture conversations have seen the evolution of several startups that provide utilities to assess credit and counterparty risks in the space.

For actors who have traditionally looked to maximize risk adjusted returns, often playing fast and loose with the perception of risk (Which I think humans are inept at judging, but more on that later), DeFi has built playgrounds that have built legos of considerable heights.

Proof-of-stake blockchains come with native yield mechanisms on existing assets, through staking yields. These generate staked tokens, usually with an unlock period. The unlock period can be waived for immediate liquidity using liquid staking, and further yield can be obtained by borrowing against staked assets, and deploying that for further yield.

While the fundamentals backing most of these yields are shaky at best, and abhorrent at the worst (we will try to evaluate how any such yield makes sense in a future blog), the game is likely to evolve in a regulated fashion.

Stay tuned for future posts exploring the mechanics of DeFi yields, emerging zero-knowledge identity solutions, and how major financial players are positioning themselves within this rapidly evolving landscape.