Back

April 16, 2025

In the early days of blockchain finance, the prevailing narrative was that base layers—protocols like Ethereum—would ultimately capture the lion’s share of value. This was the “fat protocol” thesis, famously put forward by Joel Monegro in 2016. The logic was simple: as with the Internet, where the value was embedded in the underlying infrastructure rather than the myriad of applications running on top, blockchain’s base layers would accrue most of the economic benefits. Fast forward a few years, and the stage is now shared with an emergent player: the fat app.

Over the past few years, successful decentralized applications (dApps) have rapidly garnered significant traction. From decentralized exchanges (DEXs) like Uniswap to lending platforms like Aave and derivatives hubs like GMX, these apps now boast impressive metrics in terms of total value locked (TVL), fee revenue, and user engagement. But the million-dollar—or perhaps billion-dollar—question remains: Are these fat apps merely solving for today’s incentives and hype, or do they represent a sustainable shift in value capture?

In this article, we critically examine both sides of the debate. We argue that while fat apps are indeed dazzling with their current metrics, the long-term resiliency of the crypto ecosystem may lie with protocols that provide robust interoperability and liquidity flows. In essence, the fat app thesis may be the flash-in-the-pan solution for now, while the fat protocol (or fat interoperability) thesis is what could survive the test of time.

Uniswap’s evolution is a textbook case of a fat app capturing significant immediate value. As the leading DEX on Ethereum—and now across multiple Layer-2s—Uniswap has, over time, accrued impressive numbers. In a single month in early 2024, Uniswap generated roughly $159 million in fees for its liquidity providers. That’s a volume comparable to about 6% of Ethereum’s annual fee revenue in a short period.

Uniswap’s dominance is further evidenced by its market share. It accounts for roughly 75% of all DEX trading volume on Ethereum, meaning that a single app now wields significant economic clout relative to its host chain. Even though its native token UNI doesn’t directly capture trading fees (since the fee switch is still off, but that could change soon source), its sheer scale has forced market participants to reckon with the idea that the user-facing layer is increasingly where value is created—even if the underlying fee revenue isn’t yet channeled into token appreciation.

The Uniswap story is, in many ways, emblematic of fat apps: they are where the rubber meets the road. They are built as “money Legos,” easily replicated across chains, and they drive enormous activity through high-frequency trading and liquidity provision. And yet, their reliance on massive incentives—especially in the early days of liquidity mining—raises a pressing question. If these applications lose their artificially inflated liquidity once rewards dry up, can their economic impact remain sustainable?

Take GMX as another illustrative example. GMX is a decentralized perpetual exchange that launched on Arbitrum and quickly became a star on the platform. At its height, GMX represented over 30% of Arbitrum’s DeFi TVL. During volatile periods, GMX’s fee revenue surged dramatically—one day, it posted a fee spike that rivaled the entirety of some small base chains’ fee collection.

Yet, the GMX story also carries a cautionary tale. Its remarkable performance was deeply intertwined with Arbitrum’s low-cost, high-throughput environment. And while GMX has a built-in fee-sharing mechanism that rewards token holders directly, the protocol on which it rides—Arbitrum—does not share this benefit in its own token economics. ARB, Arbitrum’s native token, is primarily a governance tool and does not capture fees. Hence, while GMX thrives by capturing user fees and rewarding its community, Arbitrum itself remains a silent partner in the background. The app’s performance is dazzling in the short term, yet it also exposes a critical structural question: if key apps can siphon off so much value from the chain, how does the underlying protocol secure long-term economic resilience? Similar questions have emerged now with Ethereum’s midlife crisis (read more here)

Aave, one of the pillars of the lending space, has established a strong presence across multiple chains. Its deployment on Polygon, for instance, is so dominant that it accounts for roughly 37–38% of Polygon’s DeFi TVL. This concentration of liquidity in a single app on a given chain underscores how a fat app can become the bedrock of an entire ecosystem’s metrics.

On one hand, Aave’s success has boosted user engagement and driven a remarkable amount of transaction volume and protocol revenue. On the other hand, its reliance on external incentives—from liquidity mining programs on chains like Polygon and Optimism—highlights the fragility of such metrics. When the yield incentives are high, mercenary liquidity flows in. But as soon as those incentives taper off, the TVL and user engagement can fall dramatically. Aave’s situation exemplifies the double-edged nature of the fat app model: while it’s capable of rapidly capturing value, much of that capture may be transient if it is not underpinned by robust, organic usage.

Across these examples, one theme recurs: much of the recent explosive growth in dApp metrics is powered by aggressive incentive schemes. Whether it’s Uniswap’s liquidity mining, GMX’s fee sharing, or Aave’s cross-chain yield farming initiatives, these mechanisms have driven a flood of “mercenary capital”—liquidity and user activity that is highly opportunistic and, by nature, short-lived.

For instance, liquidity mining programs have repeatedly demonstrated that when token rewards end, the associated liquidity and usage can evaporate quickly. The phenomenon isn’t new. During DeFi Summer 2020, a series of yield farming booms saw TVL spike dramatically, only for many protocols to witness a swift exodus of funds once the rewards dried up. More recently, initiatives like friend.tech on Coinbase’s Base network generated massive user interest via gamified incentives and point systems—but with equally dramatic subsequent cooling-off periods once the reward phase ended.

In short, while fat apps are solving the immediate problem of capturing user attention and liquidity, their heavy reliance on incentives means that their impressive metrics might not be sustainable over the long haul.

While the fat app thesis is currently riding high, there’s a counter-narrative that deserves equal consideration. The fat protocol thesis—or, as some now term it, the “fat interoperability” model—holds that base layers, by virtue of providing the essential infrastructure for all apps, have a more sustainable route to capturing long-term value.

Consider Ethereum. Despite its periodic congestion and high gas fees, Ethereum continues to generate $2.48 billion in transaction fees annually. Its design features—such as the fee burn mechanism introduced via EIP-1559—create a deflationary pressure that underpins long-term scarcity and value accrual for ETH. While individual apps like Uniswap and Aave might capture significant usage metrics, they do so on top of Ethereum’s robust and secure network. In this sense, Ethereum’s economic model is built to weather the storm of transient liquidity flows because it benefits from every transaction that occurs on its network.

Another argument in favor of the fat protocol model is the natural ebb and flow of liquidity. Base protocols are uniquely positioned to capture value from both liquidity inflows and outflows. When users flock to a dApp during an incentive-driven event, they ultimately transact on the underlying blockchain. This transaction activity—regardless of whether it’s driven by yield farming or organic use—contributes to the base layer’s fee revenue. Even if the liquidity is transient, the protocols still earn a cut through gas fees and other transactional costs.

For example, while GMX captures direct fee revenue and rewards its users on Arbitrum, the underlying network still benefits from every trade that occurs. Even if GMX’s dominance is, in part, due to fleeting incentives, Arbitrum continues to serve as the conduit for that activity. And although Arbitrum’s native token ARB doesn’t directly share in these fees, the network’s overall security and interoperability are enhanced by sustained usage—even if that usage is cyclical.

Furthermore, the case of protocols like Tron and BNB Chain provides an interesting contrast. Tron, while not a conventional DeFi hub, handles massive volumes of low-fee stablecoin transfers—resulting in fee revenues comparable to Ethereum’s daily figures. BNB Chain, on the other hand, focuses on high throughput at low cost, capturing volume rather than high fee revenue. These models underscore that while apps can capture enormous value in isolated contexts, the resilience of a protocol is measured by its ability to facilitate and monetize the entire spectrum of activity over time.

A critical aspect of the long-term argument for fat protocols is interoperability. In today’s multipolar crypto world, where applications can and do operate across multiple chains, the underlying protocols that facilitate interoperability become indispensable. A chain’s ability to attract a diverse range of dApps, while still enabling seamless cross-chain transfers and communications, is a major competitive advantage.

For instance, Ethereum’s role as the “reserve currency” in DeFi is not solely because of its high fee revenue. Its widespread adoption means that many projects—regardless of which chain they natively reside on—require ETH for settlement, collateralization, and liquidity provision. Even as apps launch on cheaper Layer-2s like Arbitrum and Optimism, they still depend on Ethereum’s security and interoperability for their broader ecosystem functions.

Moreover, emerging trends suggest that we might see more “app-chains” in the future—where fat apps start to deploy their own dedicated chains in order to capture a larger share of the value they generate. Uniswap, for instance, has toyed with the idea of launching its own “Unichain” to internalize what was previously paid out to the underlying protocol. Yet, even in these cases, the new chains will need to interoperate with established networks if they are to scale and retain value over time. In this way, the notion of a fat protocol is evolving rather than disappearing—it is transforming into a fat interoperability thesis where the base layers remain crucial as hubs that connect and validate the entire ecosystem.

At first glance, fat apps are the stars of the show. They provide compelling user interfaces, drive massive TVL inflows, and generate fee revenue that in isolated instances can rival entire blockchains. However, when we peel back the layers, it becomes clear that much of this success is tied to incentive structures that can be transient. Mercenary liquidity and one-off yield farming events create spikes in metrics that often collapse once the rewards stop. For a technical business audience looking at these numbers with a healthy dose of skepticism, the question isn’t just “What is the current TVL or fee revenue?” but rather, “How much of that value is sticky?”

The answer lies partly in the recognition that sustainable value accrues from systems that are designed to handle liquidity inflows and outflows gracefully. Base protocols, by design, are built to support a wide array of applications. They collect fees on every transaction, regardless of whether those transactions are driven by speculative incentives or by genuine economic activity. When users exit an incentivized app, the underlying protocol still reaps the benefits of the transactional activity that remains.

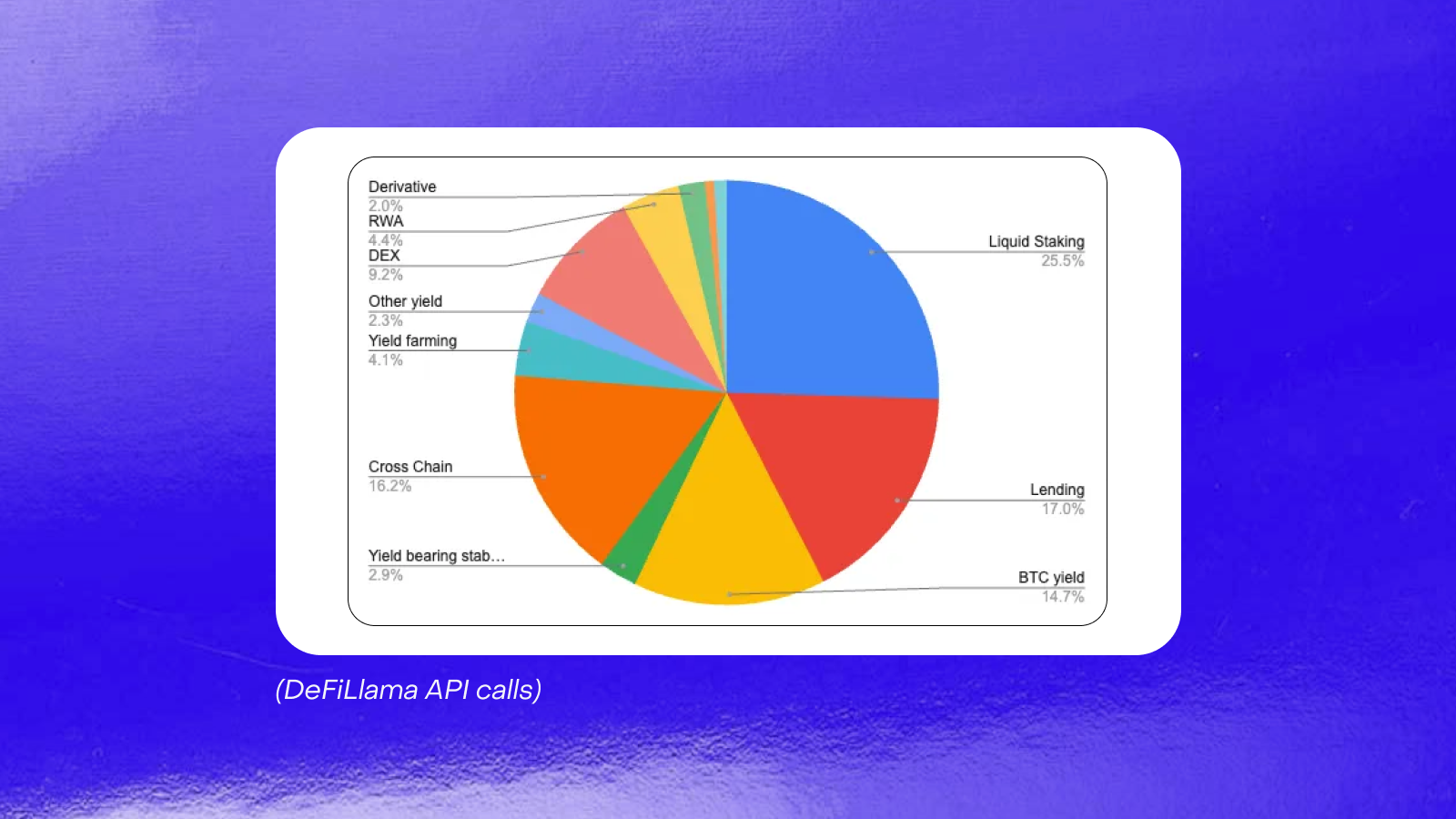

Additionally, as protocols continue to innovate—by implementing improvements like Layer-2 rollups, sharding, or even new fee models—they are positioning themselves for long-term survival. The ability of these protocols to integrate seamlessly with emerging ecosystems (think cross-chain bridges and interoperability protocols) further reinforces their enduring appeal. For instance, just bridges today account for about ~17% among the TVL of all DeFi protocols >$ 500 Mn, as evidenced in the graph below. This is further evidence of non-sticky liquidity, not just to apps, but also to protocols and L1s/ L2s. Liquidity moves with incentives, and hence remains a poor indicator of what could unlock value in 10 years.

Conversely, if fat apps are built solely on temporary incentives, their high metrics might prove to be more of a flash in the pan. The recent experience of projects that saw massive TVL spikes during airdrop or point-farming campaigns—only to see activity collapse once those incentives ended—serves as a cautionary tale. For these projects, while the narrative of being a “fat app” might seem attractive today, the sustainability of their value capture is dubious unless they can convert ephemeral hype into genuine, recurring revenue.

Looking beyond individual cases, global search trends and industry analyses suggest that the debate is far from settled. Industry giants like a16z and Paradigm are increasingly betting on multi-token strategies. Investors are now considering portfolios that mix base protocol tokens with application tokens—betting on both the network effects of foundational chains and the direct revenue capture of star dApps.

For instance, recent reports from Token Terminal show that investors are starting to use price-to-fee ratios to evaluate dApps—much like traditional companies are assessed using price-to-earnings metrics. This trend indicates that the market is beginning to see fat apps not merely as transient fads but as businesses that, if managed well, can lock in a portion of the value generated on their networks. In parallel, regulatory developments are starting to favor those projects that can prove long-term sustainability. As regulatory frameworks mature, protocols that successfully integrate compliance and interoperability may gain a competitive moat that transient, incentive-driven apps lack.

Moreover, the future may well see further integration between protocols and applications. We might see ecosystems where apps not only use the underlying blockchain but also contribute to its security or even participate in its governance and fee models. This hybrid model would effectively merge the fat app and fat protocol narratives, creating a more resilient system where value flows both upward to the base layer and laterally among applications.

In conclusion, the current crypto landscape presents us with two coexisting narratives. The fat app thesis is undeniably solving for the “now.” Applications like Uniswap, GMX, and Aave have demonstrated that they can capture impressive metrics and drive explosive user engagement—even if much of this growth is underwritten by temporary incentives. These dApps have redefined the benchmarks for success in the DeFi space and captured the market’s imagination with their explosive growth.

However, a closer, more skeptical analysis reveals that many of these metrics are built on incentives that may not be sustainable over time. When liquidity is mercenary and driven by one-off yield farming events or speculative airdrop hunts, the longevity of a fat app’s economic impact comes into question. Meanwhile, the fat protocol—or more aptly, the fat interoperability—thesis posits that the underlying infrastructure, by capturing fees on every transaction and facilitating cross-chain liquidity flows, holds the key to long-term value creation.

While the two models appear to be at odds, the reality is more nuanced. In a maturing blockchain ecosystem, both layers are interdependent. Fat apps drive user engagement and revenue, while fat protocols ensure that this activity is recorded, validated, and monetized sustainably. As industry players and investors increasingly recognize this duality, the optimal approach may lie in designing systems that blend the best of both worlds.

Ultimately, if we are to ask the question—“Where does sustainable value reside?”—the answer is not as binary as fat apps versus fat protocols. Rather, sustainable value accrues when innovative applications operate on robust, interoperable, and economically sound protocols. The immediate brilliance of fat apps may capture headlines today, but the enduring economic moat may well be built on the backbone of resilient base layers that successfully navigate liquidity inflows and outflows.

In this evolving narrative, the challenge for blockchain projects is to convert ephemeral, incentive-driven success into long-term, intrinsic value. Only then can the ecosystem mature beyond a series of speculative cycles and transition into a reliable, integrated financial infrastructure that serves both users and investors over the long haul.

In conclusion, as blockchain finance “grows up,” the market is learning that sustainable economic value isn’t solely about who can capture the most TVL or generate the highest fee revenue in the short term. It is about building systems that can gracefully handle the cyclical nature of liquidity—systems where value is not lost when incentives recede, but is instead continuously reallocated across a thriving, interconnected ecosystem. For the technical business audience monitoring these trends, the answer depends largely on the timescale of the returns that they are seeking. For a primarily hedge fund audience, the fat app hypothesis could enable the TradFi equivalent of macro based investing, driving yields and returns in the short term. For the medium term return seekers, a fat protocol thesis could make sense.

However, in the long term, my thesis is that long term value can be unlocked only by the picks and shovels that move liquidity between chains, and enable seamless transfer of value, while solving for the security of this movement.

Sources for the data and examples in this article include in-depth analyses from DefiLlama, Token Terminal, and Dune Analytics dashboards, as well as commentary from leading industry voices at a16z, Paradigm, and other crypto research firms. These diverse perspectives underpin the view that while fat apps are the stars of today’s crypto drama, the enduring resilience of blockchain finance will likely depend on robust, interoperable protocols that capture value across both liquidity inflows and outflows.